Technology & Integration

Phone, Portal, Email, IVR, Agent: Where Carriers Actually Receive Claims

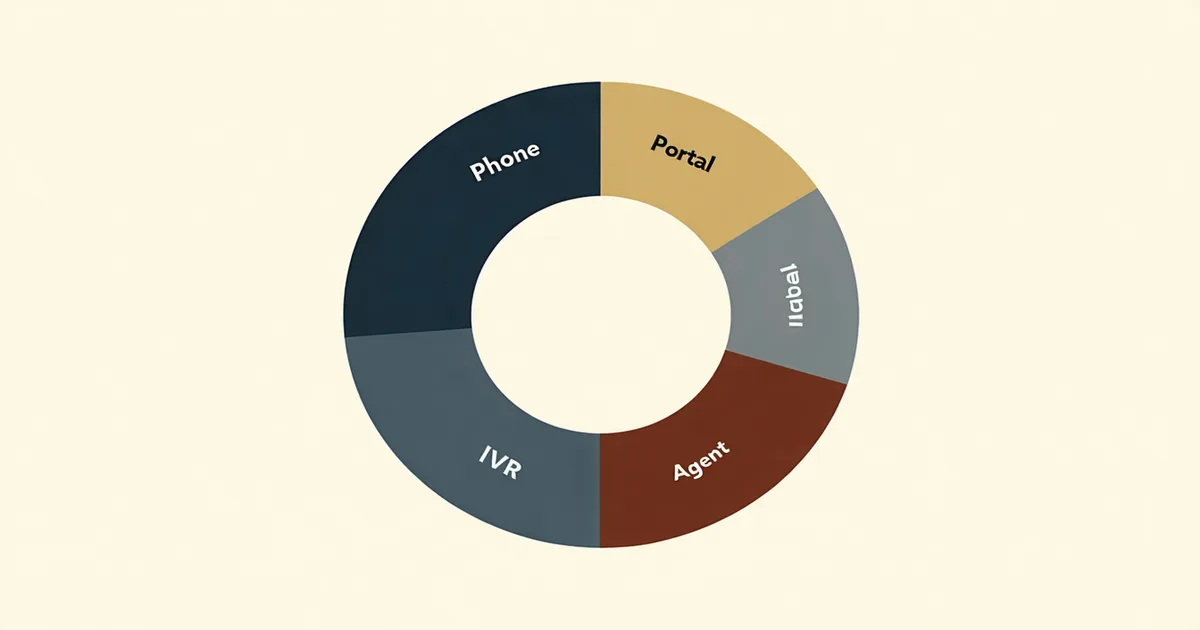

Industry data on FNOL channel mix shows phone remains dominant for commercial lines while web portal adoption has grown sharply in personal auto. Carriers running five intake channels without a common normalization layer are creating structural inconsistency in their first-contact records.