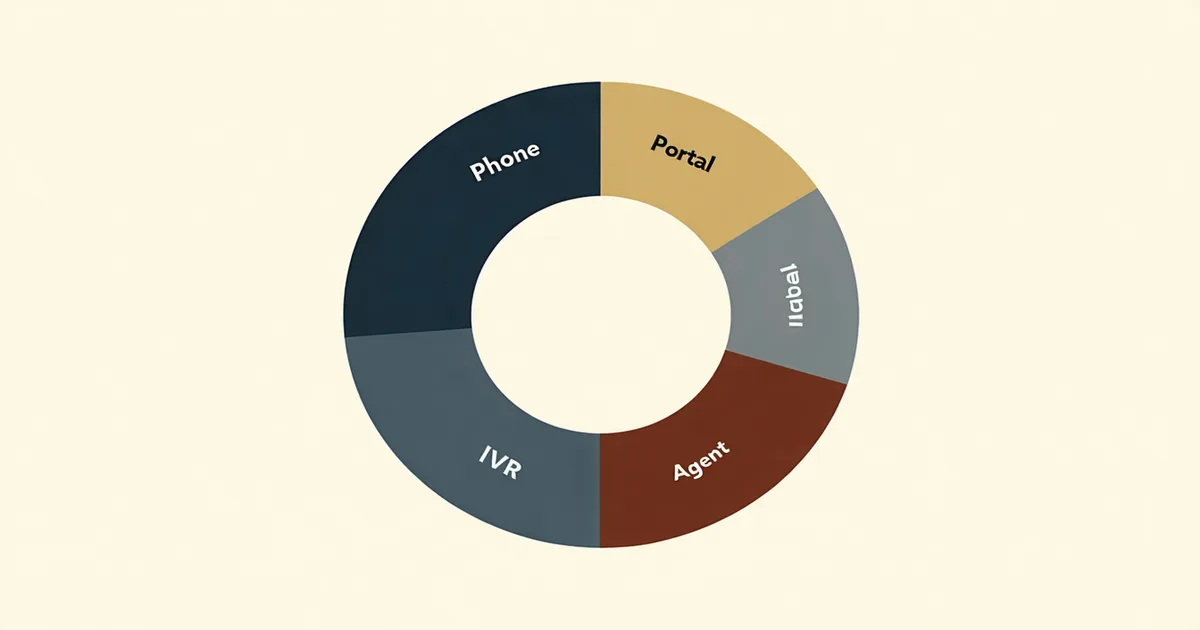

P&C carriers in 2025 typically receive first notices of loss through five or more distinct channels: a dedicated claims phone line staffed by intake representatives, an IVR (interactive voice response) system that handles after-hours and overflow calls, a web portal allowing direct claimant submission, email intake (often to a monitored claims inbox), and agent-submitted FNOLs through the agency management system. Some carriers also accept mobile app submissions and text-initiated claims for personal lines.

The channel mix is not uniform across lines of business, and it is not static. Understanding where claims actually arrive — by channel, by line, by commercial versus personal — is prerequisite to making sensible architectural decisions about intake normalization. Designing an intake system around assumptions about channel distribution that do not match the carrier's actual intake pattern produces a system that optimizes for the wrong volume and creates gaps in the channels where claims actually concentrate.

Phone: Still the Dominant Channel for Commercial Lines

Industry data from Verisk Analytics and carrier operations studies consistently shows that commercial property and commercial auto claims arrive predominantly by phone, even as self-service digital channels have matured. The reasons are operational rather than demographic: commercial policyholders — facility managers, fleet operators, risk managers at mid-market companies — are reporting losses that involve complexity, third-party exposure, or business continuity urgency that makes a phone conversation with a claims intake representative the appropriate first contact. A facilities manager at a multi-tenant office building reporting a fire suppression system activation is not going to submit a portal form; they are calling the carrier's claims line because they need a human response.

This means that phone intake quality — including the structured data-capture protocols used by intake representatives — remains the most consequential intake process for commercial lines carriers. A phone intake workflow that relies on free-text note-taking and CMS manual entry produces lower data quality than one where the representative is guided through an ACORD 1-mapped intake form with required fields. The technology challenge in phone intake is not telephony; it is the structured translation of a phone conversation into a complete, triage-ready claim record.

IVR as a complement to staffed phone intake captures after-hours FNOL volume — a meaningful share of claims, particularly for personal auto — without requiring overnight staffing. IVR intake typically captures the minimum: policy number, date of loss, callback number, and a brief description. The limitation is field completeness; an IVR FNOL rarely captures all the information needed for a triage-ready file, which means IVR records require a structured follow-up protocol to complete the intake. Carriers that count IVR submissions as "received claims" for acknowledgment-clock purposes but do not complete the file until the morning callback create an intake quality problem alongside a potential regulatory timing issue.

Web Portal: Growing Share in Personal Auto, Modest in Commercial

Web portal FNOL adoption has grown materially in personal auto lines over the past several years, driven in part by carrier investment in digital-first claims portals. A claimant reporting a personal auto collision via mobile-optimized web portal — submitting photos, entering vehicle information, and receiving an instant claim number — is using a channel that many personal lines carriers have invested in aggressively. The growth has been fastest among younger policyholders and for claim types where the loss is clearly bounded and self-documentation is feasible: fender-benders, minor collision damage, comprehensive losses like theft or vandalism.

For commercial lines, web portal adoption remains lower. Commercial auto fleet losses, commercial property damage reports, and commercial liability incidents often involve multiple parties, complex coverage questions, and business consequence that makes direct portal submission less appropriate. When a commercial policyholder uses the carrier's portal to submit an FNOL, they often submit with incomplete data — the portal was designed with personal lines use cases in mind and does not prompt for the commercial-specific fields (occupancy class, business personal property at risk, business income exposure, fleet unit number) that a commercial adjuster needs to begin investigation.

The carrier that has designed a single web portal intended to serve both personal and commercial FNOL submissions without line-specific field logic will see meaningful data completeness differences between the personal auto FNOLs that arrive fully populated and the commercial property FNOLs that arrive with empty fields where commercial-specific information should be.

Agent Submission: High Completeness, Inconsistent Format

Agent-submitted FNOLs — typically generated when an independent or captive agent on behalf of the insured calls the carrier's claims line or submits through an agency management system — tend to produce more complete records than direct claimant submissions. Agents are familiar with the information carriers need at FNOL; they often have the declarations page in front of them and can provide policy details that a direct claimant call might not capture efficiently.

The inconsistency in agent submission is format, not completeness. Agency management systems vary: some generate ACORD-structured output that integrates cleanly with the carrier's CMS; others produce email-format submissions, faxes (still used), or PDF attachments that require manual processing. A carrier receiving agent-submitted FNOLs across twenty different agency management system configurations will have twenty different intake format challenges, each requiring a different normalization approach.

We are not saying that agent submission is a problematic channel — it is often the highest-quality intake channel for commercial lines when the agency management system supports direct carrier integration. The point is that format variability is the primary quality risk in agent submission, not information completeness, and that the normalization layer handling agent-submitted FNOLs needs to account for that variability.

Email Intake: The Unstructured Channel

Email intake — whether the carrier publishes a claims email address or policyholders and agents email their agent's account manager who forwards to the carrier — is the intake channel most likely to produce unstructured, incomplete claim records. An email that says "Hi, I need to report a claim on policy number XYZ-123456 — we had a fire in the warehouse last night" contains a policy number and a loss type but nothing else required for a triage-ready FNOL.

For carriers that accept email FNOL, the intake workflow question is: who processes the email, what structured fields do they extract, and what is the protocol for obtaining the missing information? Without a defined intake protocol for email submissions, email FNOLs become a free-form queue that creates unpredictable claim file quality depending on which intake representative processes each email and how carefully they follow up for missing information.

Some carriers have addressed email intake by implementing structured acknowledgment responses — when an email FNOL is received, an automated response asks the claimant to complete a structured intake form or call the claims line. This converts the unstructured email into a structured intake without requiring the carrier to parse and interpret free-text email content.

The Normalization Problem Across Five Channels

When a carrier runs five intake channels simultaneously — phone, IVR, portal, agent submission, and email — the claim files entering the CMS do not look the same. Phone files have call notes; IVR files have minimal structured data; portal files have whatever the portal collected; agent files have the format the agency management system produced; email files have whatever the intake representative extracted from the email text. An adjuster receiving files from this mixed intake environment is constantly calibrating their expectations about what information will be present and what they need to obtain.

Normalization means establishing a minimum structured record standard — effectively an ACORD mapping requirement — for every claim that enters the CMS, regardless of channel. It means that the intake layer transforms channel-specific inputs into a consistent output structure before the claim record is written. The carrier that achieves this sees adjuster productivity gains on the back end because every file arrives at assignment with the same minimum data set present, and the adjuster's initial contact with the claimant is follow-up and investigation, not basic information gathering that should have happened at intake.

Carriers evaluating their current channel mix and intake normalization approach can speak with the Fnolwise team about how multi-channel FNOL intake can produce consistent structured records for Guidewire ClaimCenter, Duck Creek Claims, or Insurity environments.